In 1968, Dr. Martin Luther King Jr. visited the City of Newark to build support for the Poor People’s Campaign—the final phase in his fight for racial justice.

Fifty-five years after Dr. King’s visit to New Jersey, the state remains a modern-day version of the “Two Americas” he spoke of.

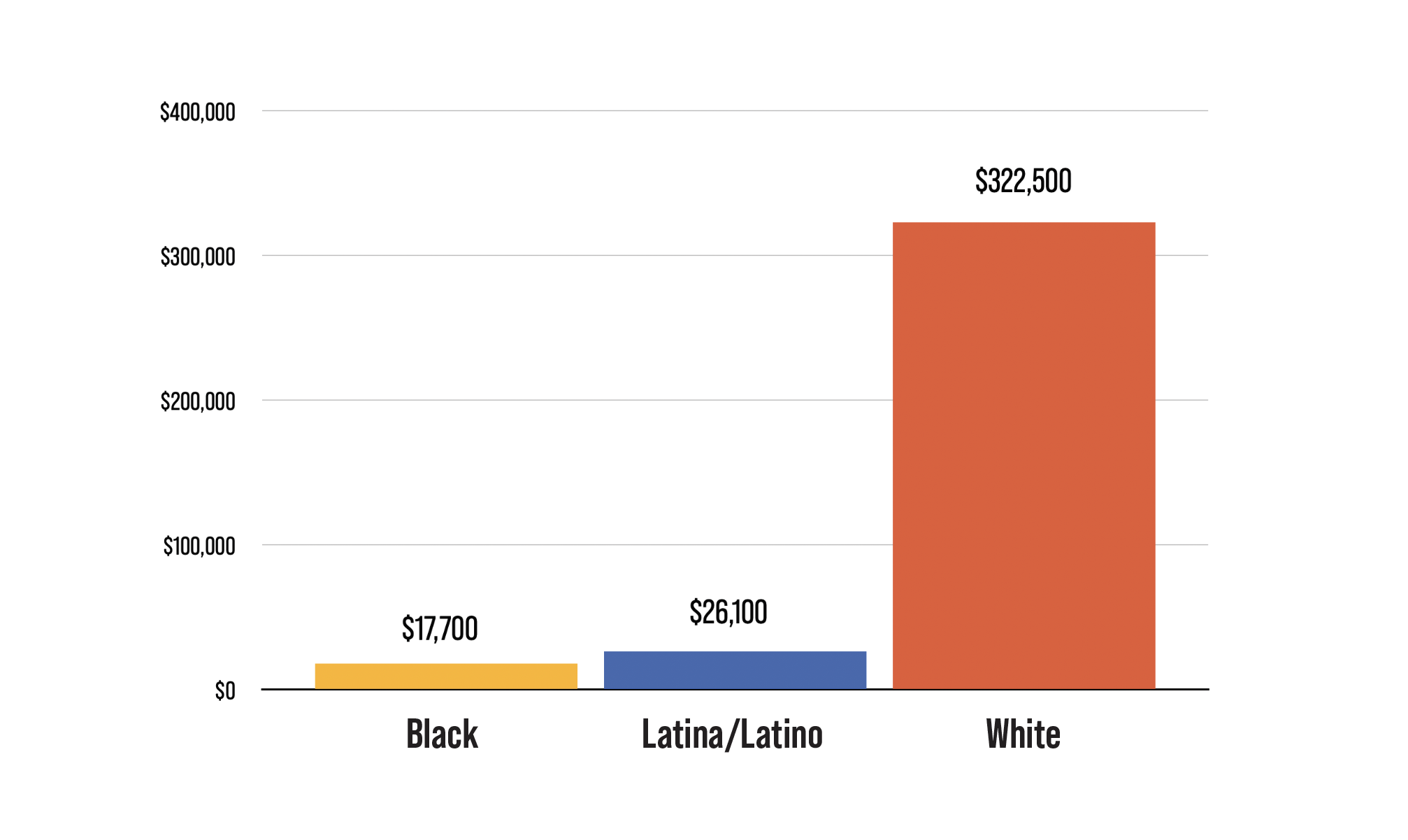

In white New Jersey, the median household wealth is $322,500.

In Black New Jersey, it is just $17,700.

This means our racial wealth gap exceeds an astounding $300,000.

The Two New Jerseys were designed during its founding when the Garden State was the “slave state of the North.” At New Jersey’s founding, colonial settlers were given an additional 150 acres of land for every enslaved person they brought with them. By 1830, over two-thirds of all enslaved people in the North were held in New Jersey. After becoming the last Northern state to end formal slavery, New Jersey developed its own form of sharecropping.

New Jersey continued its racialized system of wealth acquisition for generations, from the pervasive use of racially restrictive covenants and redlining to predatory lending.

Why does that history matter today, in 2023?

It matters because a direct line can be drawn from that shameful history to today, when Black people in New Jersey face some of the worst racial inequalities in the nation. Wealth inequality is but one manifestation.

Today, by the design of these compounding policies and practices, too many Black and other people of color in New Jersey confront substantial barriers to homeownership, are burdened by a mountain of student debt, and are excluded from quality jobs with wealth-building benefits.

It is time for New Jersey to both design and invest in a new system that connects the next generation of Black and other people of color to its vast prosperity.

While no single policy alone can close New Jersey’s staggering racial wealth gap, Baby Bonds can be a meaningful part of that investment and an essential aspect of a comprehensive strategy to provide low-income and low-wealth Black and other children of color a firm financial foundation on which to step into adulthood.

New Jersey owes it to future generations to be as intentional in connecting our young people to wealth as it has been about separating them from it.

In a Baby Bonds program, the government, soon after a child’s birth, makes an investment in an account or trust on the child’s behalf, which grows in value over time. Once the child reaches age 18, they can use the funds to finance post-secondary education, make a down payment on a home or start a small business. Baby Bonds promote equity by providing low-income and low-wealth newborns with a financial endowment for their futures—a financial head start already available to wealthy children.

Several program designs for Baby Bonds already exist around the country, with legislation passed or pending in several states and legislation introduced at the federal level.

It is time that New Jersey recognizes what other jurisdictions already have: Baby Bonds open new doors for low-income and low-wealth young people—who are disproportionately children of color—when they reach adulthood, providing them with the opportunity to build generational wealth and long-lasting economic security.

Recent research has shown that Baby Bonds could substantially reduce the racial wealth gap. Closing New Jersey’s racial wealth gap—which is nearly double that of the national racial wealth gap—requires a multi-pronged, long-term approach, and implementing a statewide Baby Bonds program for the next generation must be part of that strategy. While a New Jersey Baby Bonds program would not eliminate the racial wealth gap, it could markedly reduce it among young people, and provide greater financial stability to Black young adults navigating through barriers to wealth creation and economic success. An impactful state Baby Bonds program, ideally in combination with a federal program, would have the greatest effect in creating a more equitable distribution of wealth for the next generation.

A Baby Bonds program in New Jersey should provide larger amounts of funding to children from economically vulnerable households, who are disproportionately Black and Latina/Latino children. This would begin to address the significant disparities in wealth in New Jersey and result in greater economic equity among racial and ethnic groups over time. In this way, Baby Bonds can help reshape existing dynamics of wealth-building policies from disproportionately benefiting white people to also enabling children of color to build wealth and economic security in young adulthood.

Fortunately, there is growing awareness of the role a New Jersey Baby Bonds program could have in promoting economic justice for the next generation of Black and other people of color in New Jersey. Governor Phil Murphy proposed a statewide Baby Bonds program in August 2020 and garnered national attention for his support of the idea. Subsequently, legislation was introduced in September 2020 to create the New Jersey Baby Bonds Account Program.

The pending bill, A1579/S768, would create the New Jersey Baby Bond Account Program and Baby Bond Account Fund in the Department of the Treasury. The program would credit each infant born and residing in the state, in a low-income household, with a $2,000 deposit into an individual account within the Baby Bond Account Fund. These funds would grow in value over time, and when the child turns 18, they can use the funds for education, homeownership, small business and/or other asset-building activities.

The pending legislation provides a critical foundation for the development of a progressive, impactful Baby Bonds program in New Jersey that will meaningfully serve to open financial opportunities for young people who do not have extended family wealth. As described below, the Institute has several recommendations for strengthening the program design to ensure that the program is most effective for reducing wealth inequality and the racial wealth gap in the Garden State.

We urge the State to incorporate these recommendations and pass and sign the pending legislation into law.

Building on the thought leadership of economist Darrick Hamilton, Baby Bonds legislation has been introduced by Sen. Cory Booker and Rep. Ayanna Pressley at the federal level with the American Opportunity Accounts Act. Since then, several states and local jurisdictions have followed suit by introducing—and in some cases, passing—their own proposals to create Baby Bonds. In 2021, Connecticut became the first state in the nation to pass Baby Bonds legislation and though the program has faced some hurdles, a newly-elected State Treasurer has indicated that he is committed to implementing the program. California, Delaware, Iowa, Massachusetts, Nevada, New York, Washington, Wisconsin and the District of Columbia also have introduced Baby Bonds legislation.

In October 2021, Washington, D.C. became the second locality in the country to pass Baby Bonds legislation, entitled the Child Wealth Building Act. D.C.’s program creates a trust fund for each child born in the District after October 1, 2021, whose family participates in Medicaid and has an income of less than 300% of the federal poverty line. The fund will be credited with $500 upon the child’s birth, and for each year that the parents continue to meet income-eligibility requirements, up to an additional $1,000 will be added to the fund. Each child’s fund will accrue annually until the child turns 18 years old, at which time the child may use the total fund for wealth-building purposes, including property ownership, education, entrepreneurship or retirement investments.

In the D.C. legislation, enrollment is automatic from birth records, family contributions are not accepted to Baby Bonds accounts and the funds are explicitly excluded from asset limits in programs designed for economically vulnerable households—key design features that should inform the New Jersey program design.

Massachusetts and Washington State are among the states that may soon implement their own Baby Bonds programs and have seen substantial momentum in program development.

Last year, Massachusetts convened a Baby Bonds Task Force, which released a report in December 2022 with extensive recommendations on establishing a Baby Bonds program. The report recommends the state invest a sum of money for each baby born to a family receiving benefits from the state’s Temporary Assistance for Needy Families (TANF) program—Transitional Aid to Families with Dependent Children (TAFDC)—and each child under one year of age who is in foster care. The Massachusetts report recommended a minimum initial deposit amount of at least $6,500 to create a substantial asset by the time the child reached 18 years of age to meaningfully support wealth-building activities. Legislation to create a Massachusetts Baby Bonds program was filed in February 2023.

Washington State similarly initiated a committee to further develop its proposed Baby Bonds program—entitled the Washington Future Fund—which also issued a report in December 2022, outlining its recommendations to the Washington legislature. The report recommends investing at least $4,000 for every child who participated in the state’s Medicaid program, Apple Health, before age one, and that each child be able to utilize the funds upon reaching adulthood toward education, homeownership or entrepreneurship. Washington’s legislation has also been introduced for consideration during the 2023 legislative session and has bipartisan sponsors working with the State Treasurer in a bipartisan coalition.

The Institute has long urged the creation of a Baby Bonds program in New Jersey, including a proposal in our 2020 report, Freed from Debt: A Racial Justice Approach to Student Loan Reform in New Jersey. New Jersey was the first state to introduce Baby Bonds legislation in the nation and should build on national momentum to pass the strongest form of legislation possible. The Institute recommends the following to strengthen the currently pending bill (A1579/S768) and ensure a successful, impactful program in the Garden State:

Following D.C.’s model, making the program opt-out for those babies whose families are already connected to a New Jersey program for economically vulnerable families—such as the state’s NJ FamilyCare/Medicaid program—would reach young people automatically and significantly reduce administrative resources that would need to be dedicated to helping families sign up for the program. Finding eligible newborns based on income alone as written in the current legislation would require substantial paperwork at a busy time for families as they are adjusting to having a new baby in their families. Automatic enrollment would also reduce barriers to enrollment, such as language barriers, or lack of time or information. Research shows that opt-out programs have higher participation rates than programs that require people to opt in, particularly for low-income children, so automatic enrollment is essential to achieving the equity goals of Baby Bonds.

New Jersey’s pending legislation allows and encourages family contributions; however, this would diminish the equity focus of the program. As Baby Bonds are intended to redress the different wealth positions into which children are born due to generations of structural racism, the focus should be on providing a capital foundation for low-wealth children as they enter adulthood, not on incentivizing family savings. Families have plenty of other financial vehicles to save for their children’s futures, such as 529 accounts, and these existing savings programs already inequitably provide much greater benefits to higher-income families.

The purpose of Baby Bonds is to offer financial assistance for children’s futures, so they must not affect their household’s current economic stability and program benefits. A program design in which Baby Bonds funds are held by the government on behalf of children should not be counted as household assets for purposes of calculating other benefits. Also, legislation should explicitly include language that Baby Bonds funds are excluded from household assets that may be considered when determining eligibility for state-administered benefits programs.

While paying for postsecondary education may be a popular use of these funds amongst participants in the program, there are other designated uses of these funds, such as the purchase of a home, that typically occur beyond the age of 25. As a typical first-time homebuyer is in their mid-30s, extending the program’s eligibility for withdrawing funds by ten years will more realistically align with some participants’ goals. Furthermore, while the current legislation indicates that unclaimed funds will go to an Unclaimed Personal Property Trust Fund when participants reach age 25 if they have not claimed their Baby Bond, redirecting unclaimed funds back into the Baby Bonds program will help to increase the sustainability of the fund.

Investing in retirement is a way to acquire assets that will appreciate over time and generate wealth. Similar to D.C.’s Baby Bonds program,58 New Jersey’s program should allow for retirement investments to be an allowable use of funds. The program should facilitate moving funds into an IRA or similar retirement savings account.

As Baby Bonds are intended to enable the accumulation of wealth and help young people achieve economic mobility, the initial deposit should be substantial enough to allow the recipient to purchase an asset or invest in an education that will grow in value over their lifetime. In order to determine how much investment is needed to ensure children have sufficient funds when they reach adulthood, New Jersey must consider the future costs of mobility and wealth investments in the state, such as paying for postsecondary education or buying a home. Massachusetts’s report on Baby Bonds, which outlined a comprehensive model detailing various endowment sizes with 18-30 year estimates for the funds and annual costs, can serve as a model for this analysis.

The need for a sustainable funding source is crucial for the long-term sustainability and impact of the program. Cannabis social equity tax revenues which must be directed towards programs that promote social equity are an important option that the legislature should consider. Additionally, several other options exist for generating revenues to be directed toward the New Jersey Baby Bonds program. Remaining American Rescue Plan (ARP) funds—of which several billion dollars are remaining, according to the Governor’s Disaster Recovery Office—could also be used to get the program established. As ARP funds were designed to support economic recovery and security after the pandemic, particularly for the most vulnerable, using them to reduce the racial wealth gap would align with the intended use of the funds.

While Baby Bonds will provide substantial financial assistance in helping young people purchase wealth-generating assets, they will not provide each participant with enough funds to fully finance their asset goals. Therefore, participants will need access to support and education to achieve their economic objectives as they transition to adulthood, such as completing post-secondary education or making mortgage payments on a home. The Baby Bonds program should include engagement with parents and Baby Bonds participants throughout the participants’ early life and up until they turn 18 years of age, leveraging pre-established partnerships with state agencies such as the Department of Health and Department of Education, as well as trusted community-based organizations.

Baby Bonds are an important step for closing the racial wealth gap and investing in a more equitable future for New Jersey. The racial wealth gap has been created through generations of racist policies and practices, and thus, closing it will require several policy solutions working in tandem. The establishment of a New Jersey Baby Bonds program is a crucial step toward equity for the next generation. Investing in Baby Bonds will have ripple effects for young people across the Garden State that will help them to achieve their potential while also helping to reduce wealth inequalities.

Fifty-five years after Dr. King’s visit to New Jersey, it is time to make investments in our young people that allow them to thrive. Let’s fund our future.